Pre-Deposit Report: Plasma Raised $1.8B in Pre-Deposits. Here's What Actually Stayed

Retention Report is a research series that analyzes onchain capital formation campaigns on what matters: 90-day retention, not launch-day headlines.

Why This Series Exists

The crypto industry has a measurement problem.

A chain raises $2B in pre-deposits. TVL hits $8.4B in ten days. The founders tweet. The VCs celebrate. CoinDesk writes the headline. And then nobody checks back in 90 days to ask: did any of it stay?

This series does.

Retention Report exists because launch-day TVL is a vanity metric. It tells you how much capital showed up for the party. It tells you nothing about how much stayed to build. The only number that matters is retention — measured in stablecoins, measured at 90 days, measured against the baseline, not the peak.

Plasma is Report #001 because it's the largest pre-deposit campaign in crypto history. $1.8B+ raised across four rounds. Backed by Tether, Bitfinex, and Peter Thiel. 100+ protocol integrations on day one. If any campaign should have delivered durable liquidity, it was this one.

That makes it the perfect benchmark to test a thesis: it's not the size of the pre-deposit that determines retention. It's the incentive architecture around it.

The Framework: Why 90 Days

This series uses a three-checkpoint model:

- Day 0 (Launch): Baseline metrics. What landed on-chain when the doors opened?

- Days 1–15 (Peak): Maximum mercenary inflow. How much hot capital rushed in to farm launch incentives?

- Day 90 (Retention): The reality check. One full business quarter. Long enough for farming cycles to complete, token unlocks to hit, and hype to fade. Short enough to be actionable.

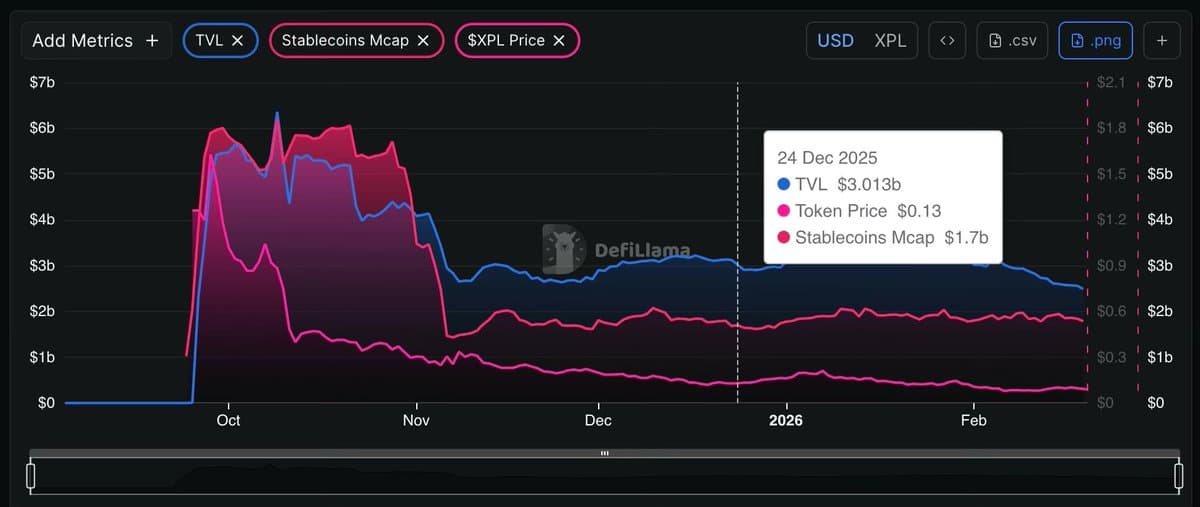

For Plasma: Day 0 was September 25, 2025 (TGE). Peak was ~Day 10 (early October). Day 90 was December 24, 2025.

The Setup: $2.55B Before a Single Block

Plasma didn't launch cold. By TGE, it had already executed one of the most aggressive pre-deposit sequences the industry had ever seen:

- June 12, 2025: $1B raised in 30 minutes.

- July 28, 2025: $373M public sale, 7.4x oversubscribed.

- August 20, 2025: $250M Binance Earn, filled within an hour.

- August 22, 2025: Binance Earn cap increased to $1B.

- September 16, 2025: $200M Maple vault, filled before the public UI even launched.

- September 19, 2025: $250M USD.Ai pre-deposit launched.

Total pre-TGE deposits: $2.55B (excluding the public sale).

The narrative was at maximum strength. Plasma positioned itself as the first blockchain to enable zero-fee USDT transfers — a payments infrastructure for the world, backed by Tether itself, with 1,000+ TPS and sub-second finality.

Users had locked capital for 3–5 months. The Maple vault filled through direct smart contract deposits before most people even saw the UI. Community anticipation was at a fever pitch. Major exchange listings — Binance, OKX, Bybit — were confirmed for day one.

The question wasn't whether the launch would be big. It was whether the capital would stay.

The Mechanics

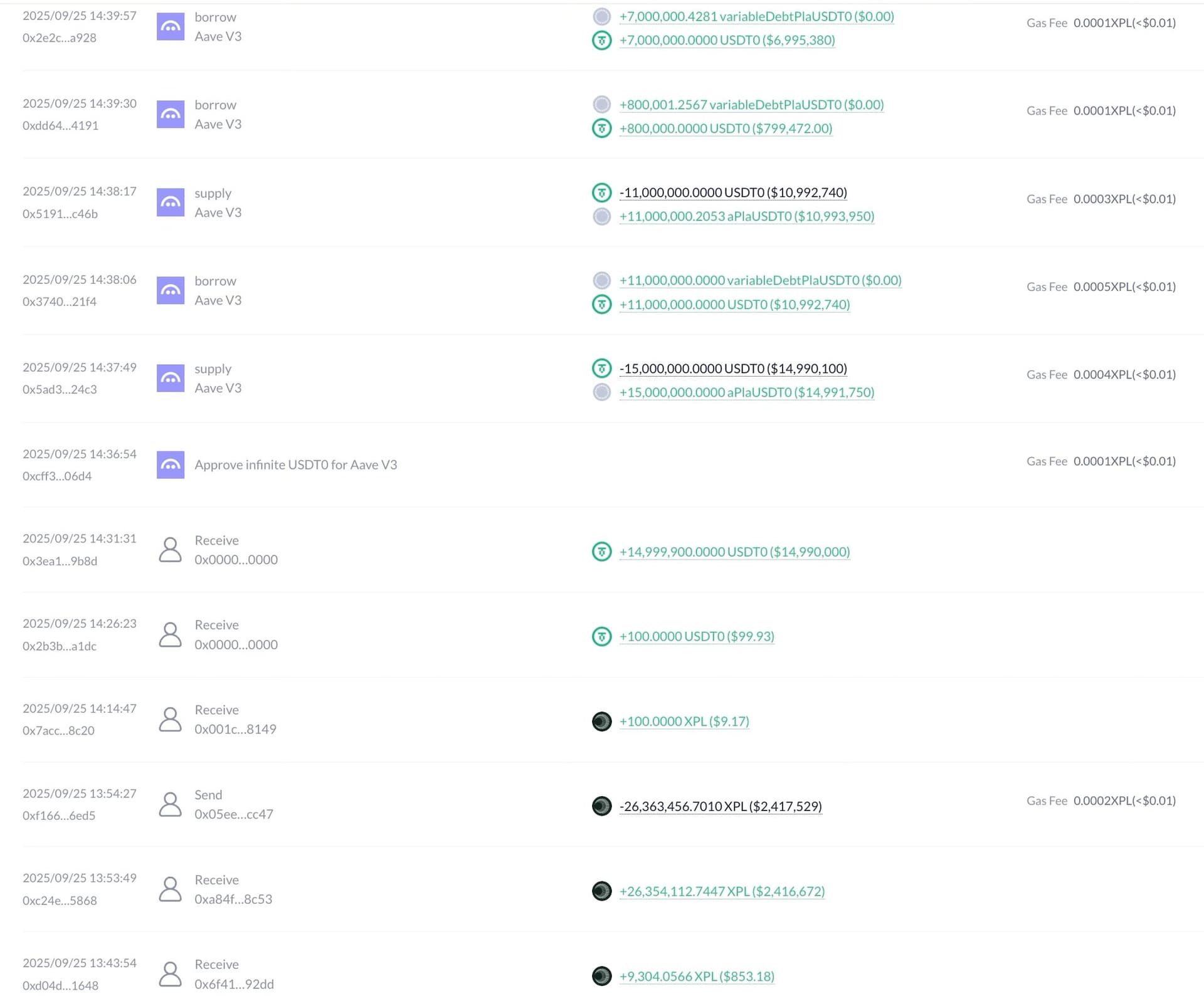

Phase 1: Deposit Period (June 2025). Participants deposited USDT, USDC, USDS, or DAI into Veda vault contracts on Ethereum mainnet. Deposits were deployed into Aave and Maker, earning a base yield of 3–6% APY. Users earned time-weighted "units" — a metric determining their allocation in the upcoming public sale. Withdrawals were possible but forfeited all accumulated units.

Phase 2: Lock-Up (40+ days). Once deposits closed, vaults locked. All stablecoins were converted to USDT. Minimum 40-day lock-up with no deposits or withdrawals.

Phase 3: Public Sale (July 17–28, 2025). 10% of total supply (1,000,000,000 XPL) sold at $0.05 per token ($500M FDV). Crucially, allocations were proportional to units earned — bigger deposits held longer earned larger guaranteed allocations. Participants committed separate, new capital to purchase their XPL; the vault deposit was not used for the purchase and was returned in full.

Phase 4: TGE & Mainnet (September 25, 2025). Vault deposits bridged to Plasma as withdrawable USDT. Token distributions executed. XPL launched at $1.26.

TGE Day: September 25, 2025

Initial metrics at launch:

| Metric | Value |

|---|---|

| TVL | $2.05B in stablecoins |

| XPL Launch Price | $1.26 |

| Market Cap | $1.8B–$2.25B |

| FDV | ~$10B |

| Circulating Supply | 1.8B–2.25B XPL |

The Two-Layer Distribution

Plasma had two separate XPL distributions on TGE day. Understanding both is critical to understanding what happened next.

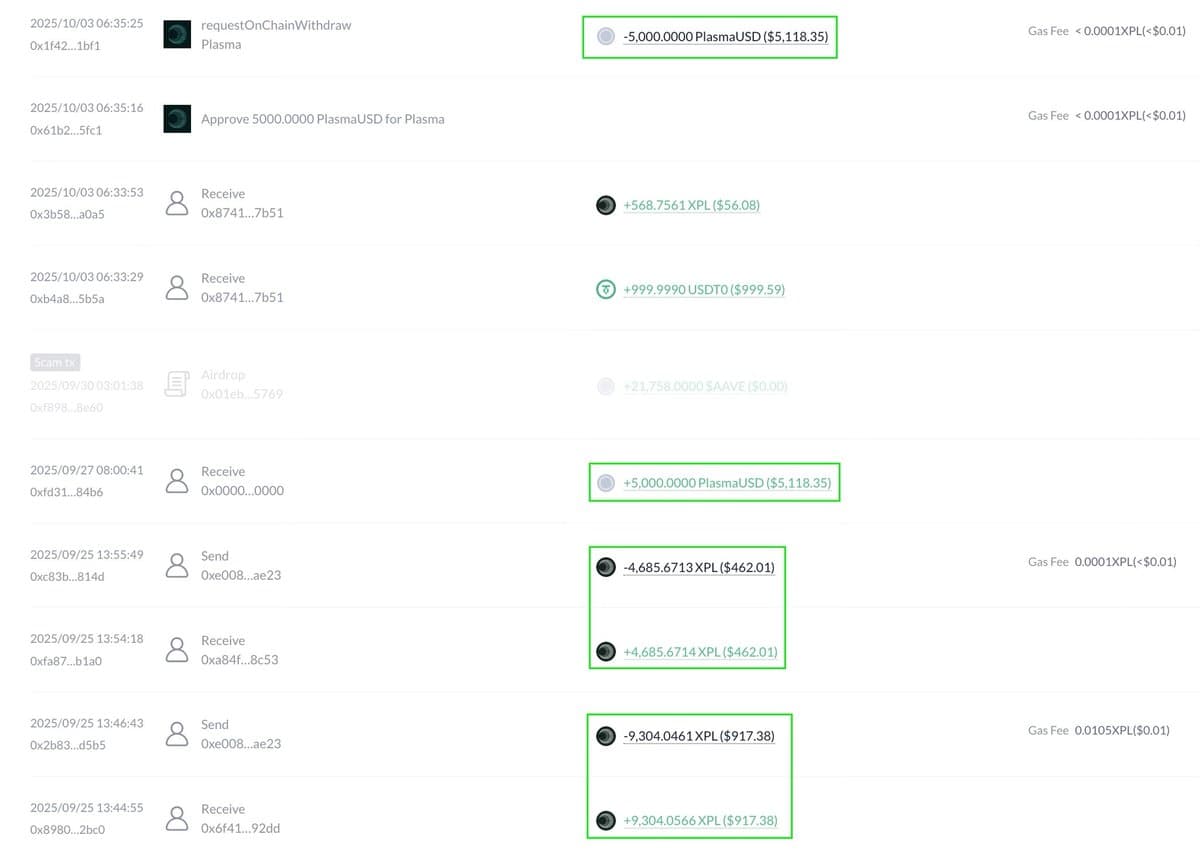

Layer 1 — The Airdrop (25M XPL, $28.3M at 3-day TWAP): Every verified participant received ~9,304 XPL ($10,541 at TWAP), regardless of deposit size. This was egalitarian — a $5K depositor got the same as a $15M depositor. Cost basis: $0.

Layer 2 — The Public Sale (1B XPL, 10% of supply): Allocated proportionally based on time-weighted vault deposits. Price: $0.05 per XPL. Participants committed separate capital to purchase their allocation. A whale with $23M in deposits received 22M+ XPL; a $500K depositor received ~541K XPL. Cost basis: $0.05/token.

The lockup terms: Non-US purchasers received XPL fully unlocked at mainnet — zero lockup, zero vesting, immediate liquidity. US purchasers had a 12-month lockup. This distinction is critical: the majority of public sale participants could sell everything immediately.

The Fatal Flaw: Zero Friction on Exit

The egalitarian airdrop created dump pressure from small wallets — free $10K with no structural reason to hold at any price. The proportional public sale gave whales massive allocations at $0.05 with zero lockup, making immediate sale at $1+ for a 20–25x return the rational economic move. No participant at any tier had a structural incentive to hold.

- Small depositor received 9,304 XPL ($10,541) from the airdrop + ~4,686 XPL ($5,309) from public sale for pre-depositing $5K. Massive profit, no reason to wait. Immediate dump.

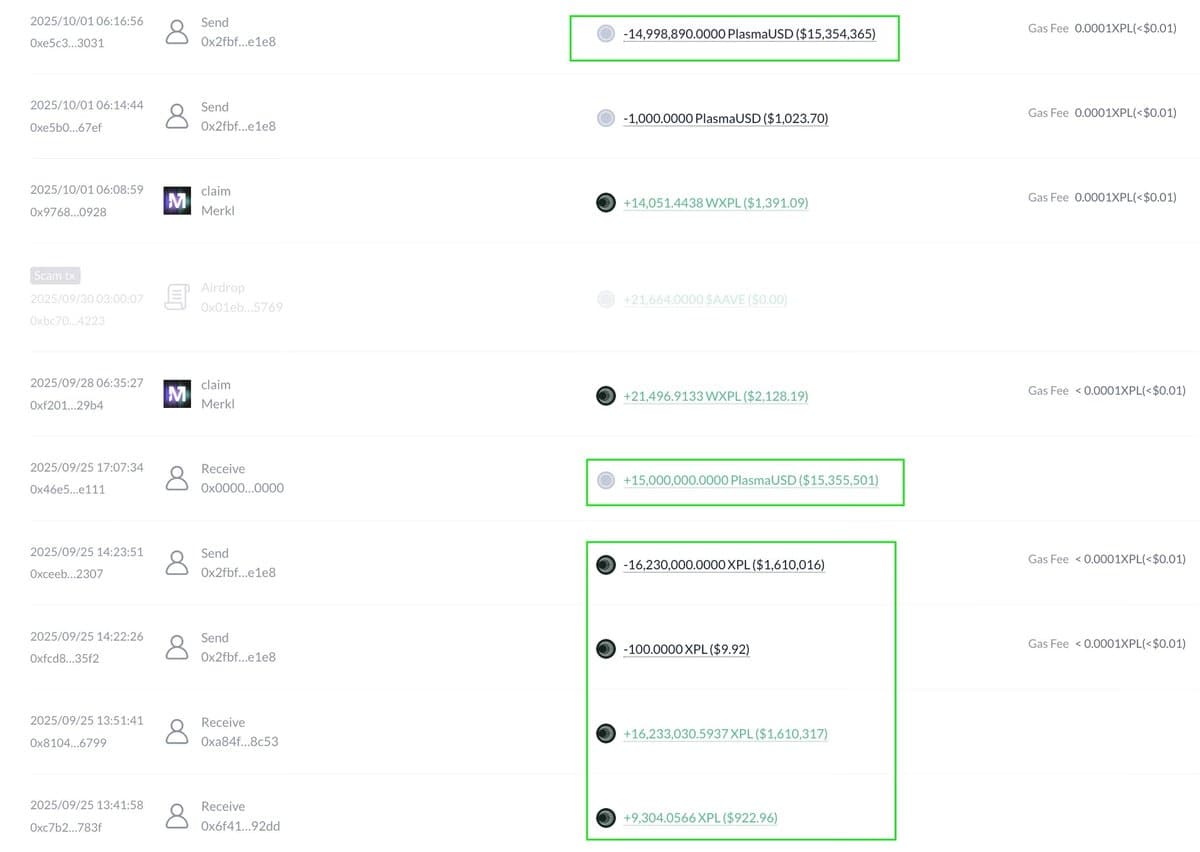

- Large depositor received 9,304 XPL ($10,541) from the airdrop + 16,233,030 XPL ($18,392,023) from public sale for pre-depositing $15M. They made a massive return. They still dumped everything — not because they were undercompensated, but because there was nothing stopping them.

Result: maximum sell pressure from small wallets (free airdrop tokens) + maximum capital extraction from large wallets (20–25x public sale returns with zero lockup).

Participant Performance: 378% Net APY

Actual Wallet Performance Data

Four wallets representing $27.56M in total pre-deposited capital were analyzed. All participated in both the airdrop and the public sale. Net APY accounts for the cost basis of the public sale purchase — the pre-sale capital committed is subtracted from XPL value to calculate actual profit.

Average Net APY: 378.5%

APY calculated as: (Base Yield + XPL Value at TWAP − Pre-Sale Cost − Gas Fees) ÷ Pre-Deposit Amount × (365 ÷ Duration). The 3-day post-TGE TWAP of $1.133 is used for XPL valuation. The pre-deposit amount (not total capital including pre-sale) is used as the denominator, consistent with the convention that the deposit earned the right to purchase at $0.05 and the pre-sale capital was a separate commitment.

Primary return driver: Pre-sale at $0.05 vs. $1.133 TWAP — a 22.66x multiple on the token purchase.

Example: Wallet #3 Breakdown

Capital committed: $2,300,000 pre-deposit (locked 108 days) + $125,224 pre-sale purchase = $2,425,224 total.

Returns at TGE: Base yield: $21,186. Original deposit returned in full: $2,300,000. Airdrop: 9,304 XPL = $10,541. Pre-sale tokens: 2,504,484 XPL = $2,837,592. Total value: $5,169,319.

Net profit: $2,837,592 + $21,186 + $10,541 − $125,224 − $577 gas = $2,743,518. ROI: 113.1% on total capital. Net APY: 402.6%.

Day One Ecosystem: A Farming Casino

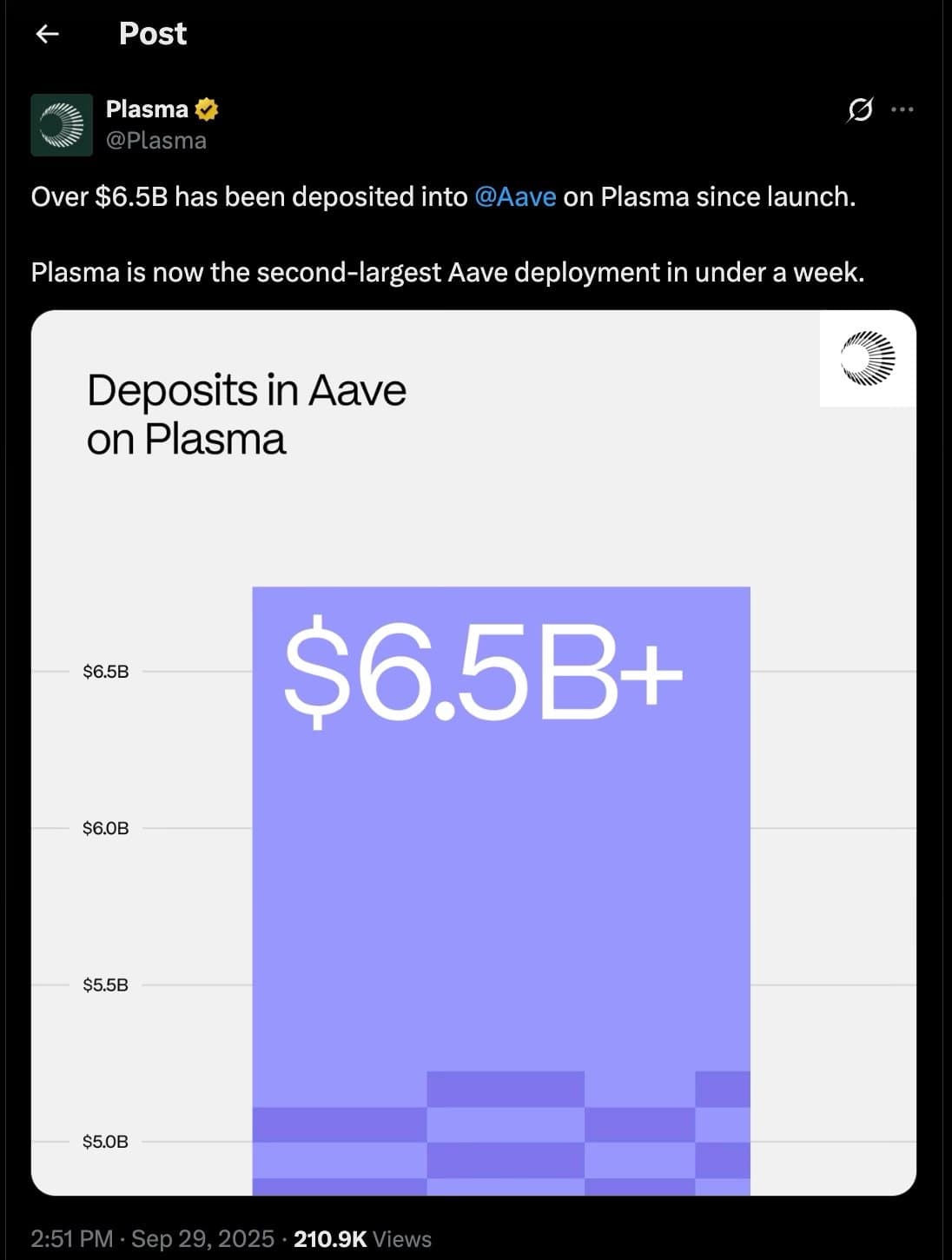

On launch day, Plasma went live with integrations to over 100 DeFi protocols — Aave, Compound, Euler, Radiant, Pendle, EtherFi, Renzo, Ethena, Uniswap, Aerodrome, Velodrome, Fluid, Gearbox, and more.

This created a powerful yield farming environment from hour one. Users could deposit USDT on Plasma, route it into Aave or any approved protocol, earn 20%+ APY in XPL rewards, and withdraw at any time. No lockup. No commitment. Full liquidity.

In practice, this wasn't a payments infrastructure stack delivering real-world USDT transfers. It functioned as a high-intensity yield farming environment, optimized for short-term extraction rather than sustainable payment usage.

Days 1–10: The Mercenary Surge

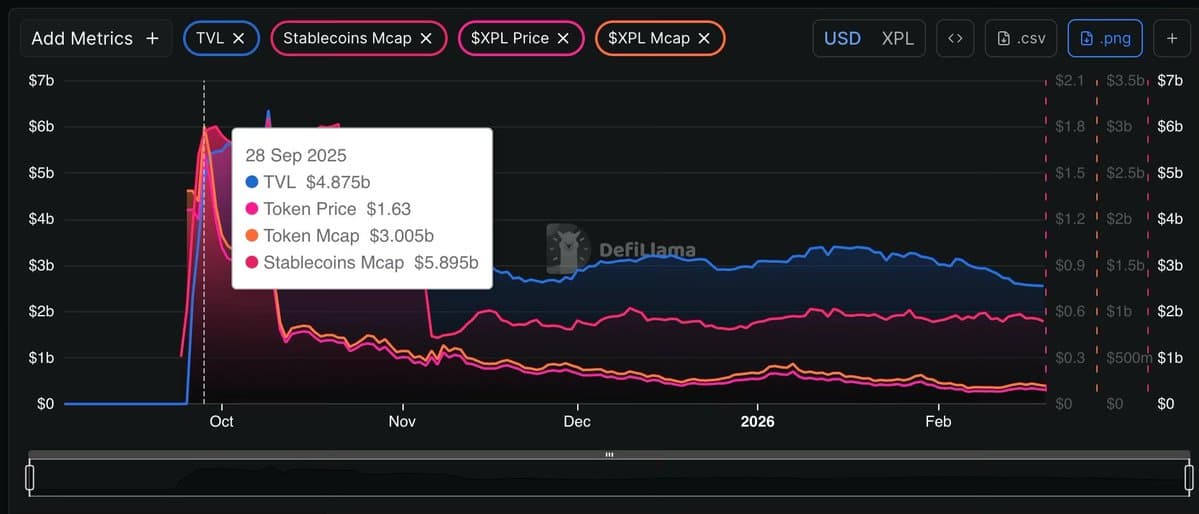

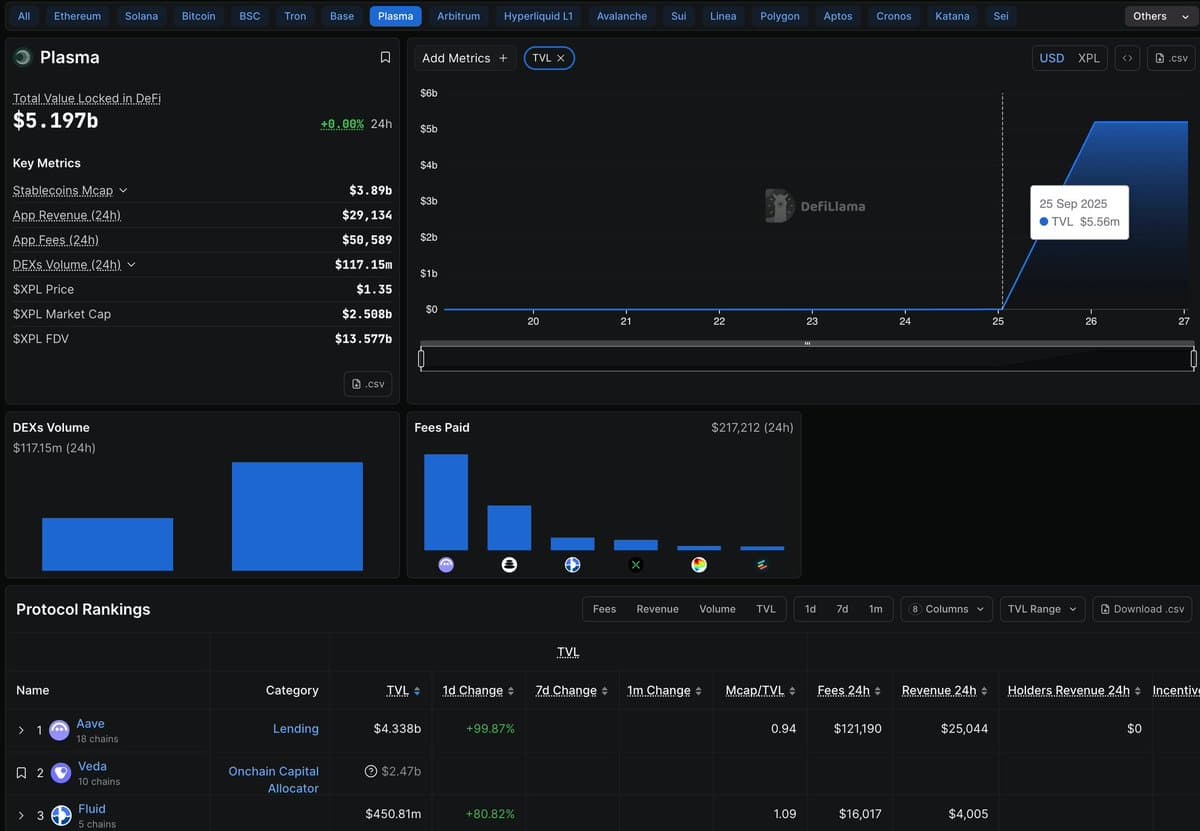

In just ten days, $6.35B in new capital flooded into Plasma. TVL hit $8.4B — a 309% increase from launch.

Peak metrics:

| Metric | Value |

|---|---|

| TVL | $8.4B |

| XPL Price (Day 3 ATH) | $1.68 |

| Stablecoins on-chain | $6.3B |

| Market Cap | ~$3.8B |

The Aave Meta

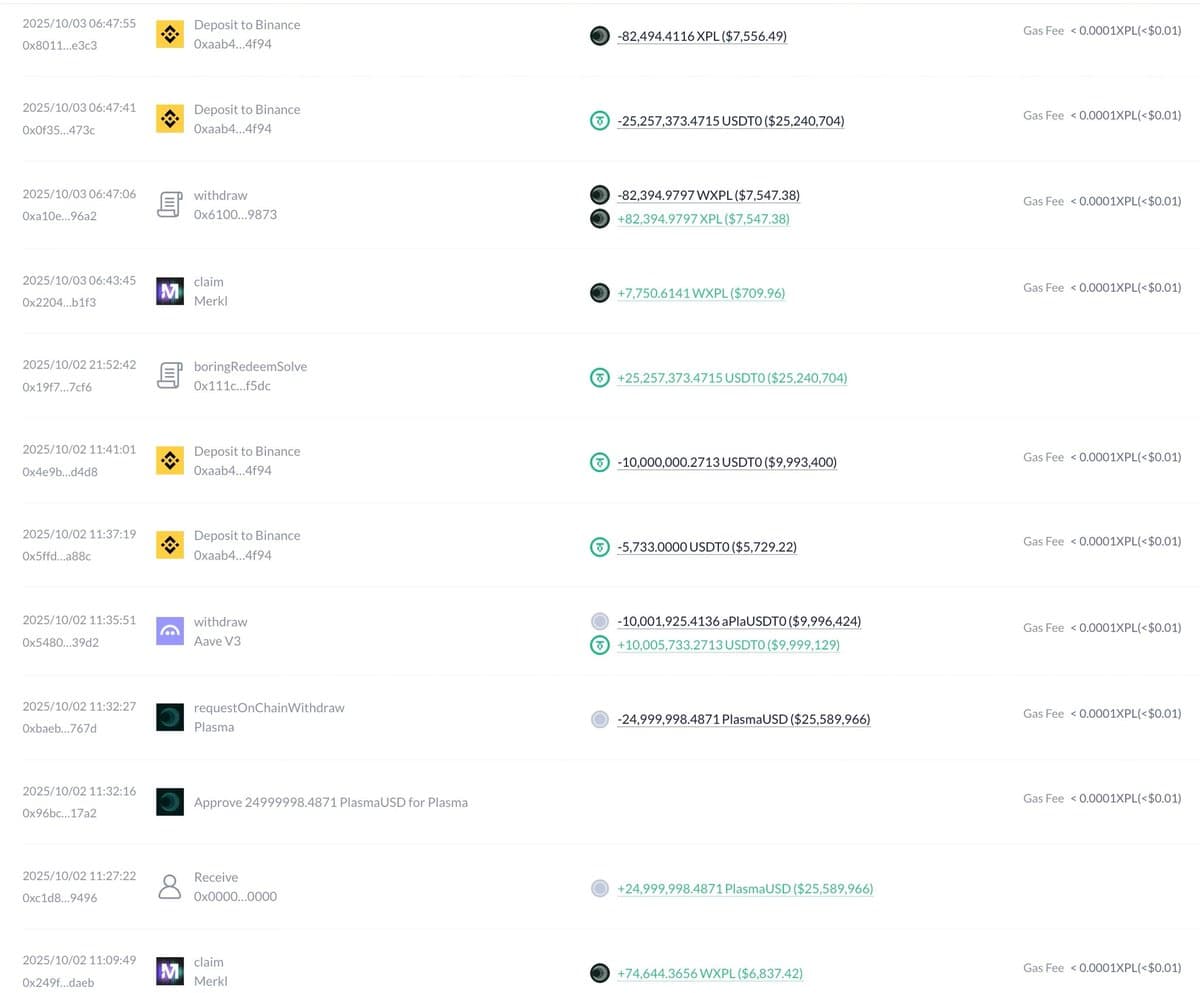

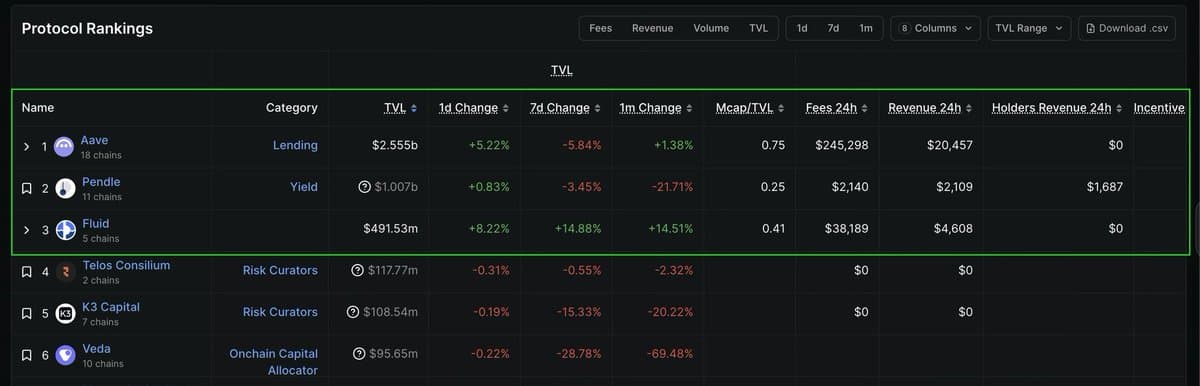

Aave on Plasma absorbed $6.6B — roughly 79% of the entire chain's TVL. The playbook was simple: deposit USDT → supply to Aave → earn 20%+ APY in XPL → sell XPL daily → compound or withdraw. No commitment required.

Capital distribution across Plasma at peak:

| Protocol | Share of TVL |

|---|---|

| Aave | 60–70% |

| Pendle | 10–15% |

| Fluid | 5–8% |

| Other | 10–15% |

Stablecoin supply at peak: $6.2B — 65% in Aave lending vaults, 20% in Pendle/Fluid/Ethena yield optimization, 15% in wallets, DEXs, and other protocols.

Why Price Peaked at $1.68, Then Immediately Reversed

Launch FOMO and speculative demand from exchange listings drove early buying. Some farmers held XPL short-term for governance positioning. And the airdrop sell pressure hadn't fully materialized yet.

Then the sell-side caught up: 25M XPL airdropped at zero cost basis (pure profit at any price), daily farming emissions (~1M+ XPL/day) sold by professional farmers, no organic buy demand for XPL (governance token with unclear utility — payments happen in USDT), and profit-taking by early speculators.

The $6.35B surge was not organic adoption. It was professional capital chasing 20%+ APY with zero commitment and full exit liquidity.

Day 90: December 24, 2025 — The Truth

| Metric | Day 90 Value | vs. Launch | vs. Peak |

|---|---|---|---|

| TVL | $3.013B | +47% | -64% |

| XPL Price | $0.13 | -87% to -90% | -92% |

| Stablecoins | $1.7B | -17% | -73% |

| Market Cap | ~$234M | -88% | -94% |

What Stayed, What Left

The Exodus. From peak to Day 90, $5.39B in TVL departed — a 64% decline. The $6.35B that flooded in during Days 1–10 almost entirely left. The stablecoin picture is even clearer: $4.6B in stablecoins exited from peak, a 73% decline. This wasn't capital rotating between protocols on-chain. It left the chain entirely.

What Remains. The $3.013B TVL at Day 90 breaks down roughly as:

- ~$2.052B: Original pre-deposit capital that largely stayed

- ~$961M: Net new capital that remained (+47% growth from baseline)

But this "growth" comes with asterisks. 80% of the remaining TVL was still concentrated in Aave farming loops. The token had lost 90%+ of its value. And stablecoins were still bleeding — down 17% even against the original pre-deposit baseline.

Protocol Concentration at Day 90

| Protocol | TVL | Share |

|---|---|---|

| Aave | ~$2.4B | 80% |

| Pendle | ~$300M | 10% |

| Fluid | ~$180M | 6% |

| Other | ~$133M | 4% |

Still 80% in Aave. After 90 days, 100+ protocol integrations, and $28.3M in airdrop incentives distributed, Plasma's "ecosystem" was still functionally a single Aave deployment.

The Retention Math

Incentive Cost

Plasma's capital formation involved two incentive layers, each with a different economic character:

- Airdrop: $28,325,000 (25M XPL × $1.133 TWAP). This was a direct cost — tokens distributed for free to participants, diluting existing holders.

- Pre-Sale Discount: ~$1,083,000,000 (1B XPL × ($1.133 TWAP − $0.05 sale price)). This represents the implicit opportunity cost of selling 10% of supply at $0.05 when the market opened at $1.13+. It's not cash out of pocket — Plasma received $50M in sale proceeds — but it's the difference between what they received and what those tokens were worth at launch. Whether to count this as an "incentive cost" depends on methodology; it's included here for completeness but the two figures are kept separate throughout.

Cost of Liquidity (COL)

Using direct incentive cost (airdrop only):

| Metric | Value |

|---|---|

| Per $1 of 90-day TVL | $0.0094 (0.94 cents) |

| Per $1 of net new capital | $0.0295 (2.95 cents) |

| Per $1 of stablecoin retained | $0.0167 (1.67 cents) |

Using total incentive cost (airdrop + implicit pre-sale discount): Per $1 of 90-day TVL = $0.369 (36.9 cents).

The stablecoin-denominated metric ($0.0167 per $1 of stablecoin retained) is the most honest of these numbers. TVL is inflated by token-denominated positions whose value fluctuates with XPL price; stablecoins are real capital with a stable dollar value.

TVL Retention Rates

- From launch to Day 90: 147% (appears to show growth — $2.052B → $3.013B)

- From peak to Day 90: 36% (64% of capital fled — $8.4B → $3.013B)

The +47% "growth" from launch is almost entirely the original pre-deposit base staying put. The -64% decline from peak reveals the actual story: nearly all mercenary capital exited within a quarter.

Stablecoin Retention — The Real Signal

- From launch to Day 90: 83% retention ($2.052B → $1.7B, 17% left)

- From peak to Day 90: 27% retention ($6.3B → $1.7B, 73% fled)

Stablecoins tell the truth that TVL obscures. While headline TVL showed +47% growth, actual stablecoin capital was down 17% from launch. Some of the original committed capital left too — partially replaced by token-denominated TVL inflated by XPL positions. Real capital outflow was worse than the TVL number suggests.

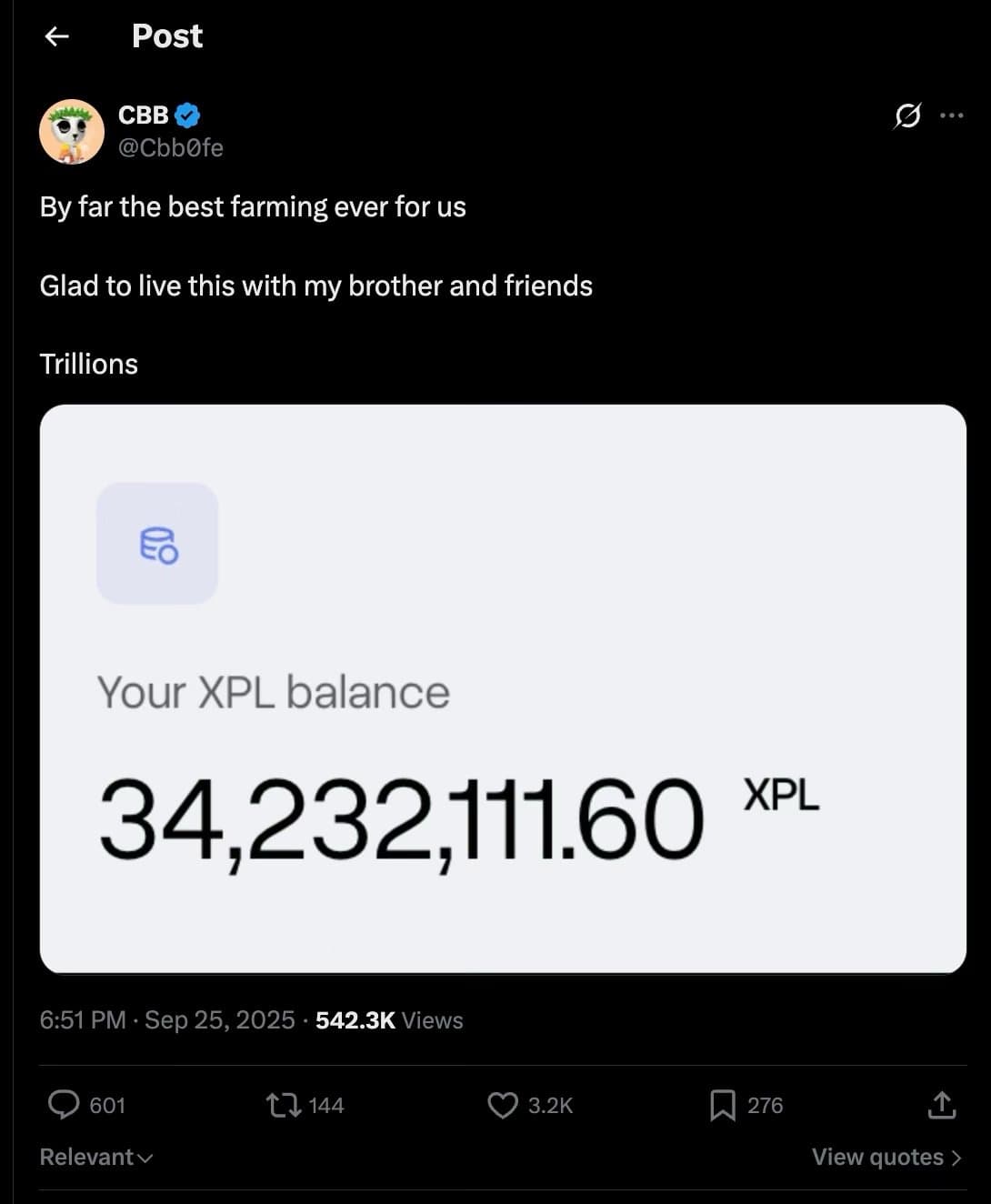

The Farmer's Perspective

The professionals knew exactly what they were doing. This whale publicly documented the playbook on TGE day:

The 34.2M XPL balance was almost entirely a public sale allocation — purchased at $0.05/token with separate capital (estimated ~$1.71M cost basis), funded by a large pre-deposit position that earned correspondingly large unit allocation. The pre-deposit itself was returned in full as USDT on Plasma. Four days later, 90% sold at $1.43 average: ~$44M in proceeds from ~$1.71M in token purchase capital. Roughly 25x return.

"Best farming ever" = deposit stablecoins for a few months (returned in full), earn the right to buy XPL at $0.05, sell at $1.43 four days after TGE. Zero lockup made this the rational play. The chain absorbed the sell pressure. Token holders absorbed the loss.

This is what zero-friction exit produces. Not communities. Not ecosystems. Extraction events.

The Verdict

Plasma raised $2.05B in pre-deposits. Most of it stayed.

The pre-deposit primitive did its job. Capital was committed months in advance, locked through a defined period, bridged to mainnet at TGE, and largely remained on-chain at Day 90. 83% stablecoin retention from the pre-deposit baseline is a strong result. That part worked.

What failed was everything around it.

Zero post-TGE lockup on public sale tokens for non-US participants — allowing immediate 20–25x extraction. An egalitarian airdrop that paid $5K wallets the same as $15M allocators, creating dump pressure across every tier. Unrestricted Aave farming at 20%+ APY that attracted $6.35B in mercenary capital with no retention mechanism. And a governance token with no organic demand, creating a one-way sell pressure valve that destroyed 92% of token value in 90 days.

The result — 64% TVL decline from peak, 92% token price destruction, 73% stablecoin exodus from peak, 80% concentration in a single farming protocol — was not a failure of pre-deposits. It was a failure of incentive architecture.

The data suggests the pre-deposit model produces better outcomes when paired with tiered allocation (reward proportional to commitment), post-TGE lockup or vesting mechanics, structured deployment through curators instead of open-access farming, and incentive designs that reward capital that stays — not just capital that shows up.

Plasma had none of these. It had size, hype, and backing. And it proved that none of those things substitute for structural design.

Pre-deposit structure — caps, tiered allocation, lockup mechanics, curator mandates — matters more than pre-deposit size.

Methodology

Data Sources: DefiLlama (TVL, stablecoin supply — primary source). CoinMarketCap (XPL 3-day TWAP post-TGE, price data). On-chain explorers / Etherscan / Plasmascan (wallet transactions, token distributions). Official Plasma announcements (campaign details, sale terms, distribution schedules).

Analysis Period: September 25, 2025 (Day 0) → December 24, 2025 (Day 90)

Key Metrics Tracked: TVL (launch, peak, 90-day), XPL price (launch, ATH, 90-day), stablecoin supply (on-chain), protocol concentration, wallet-level transaction flows.

APY Methodology: Net APY calculated using the 3-day post-TGE TWAP of $1.133 for XPL valuation. Public sale cost basis (capital committed at $0.05/token) is subtracted from XPL value before computing returns. Pre-deposit amount used as denominator. Gas fees deducted.

Cost of Liquidity Methodology: Two incentive layers reported separately. Airdrop cost ($28.3M) is a direct dilutive cost. Pre-sale discount (~$1.08B) represents implicit opportunity cost — the difference between the sale price and TWAP at launch — and is reported for completeness but not conflated with direct spend. Stablecoin-denominated TVL used as the preferred retention metric over headline TVL, which includes volatile token positions.

Analysts: Yield Network, February 2026

What's Next

Retention Report #002 is in progress. Every major capital formation campaign deserves a 90-day follow-up. The track record builds one report at a time.

Follow @maxyamp and @yield_network for the next report.

This report is for informational purposes only and does not constitute financial advice. All data is sourced from publicly available information and is believed to be accurate at the time of publication.